One of the recurring questions about Bitcoin is whether it can ever become a widespread money, when its purchasing power is expected to increase over time. I have written about such matters (with my co-author Silas Barta) in this free guide, but it will be helpful to frame the issue in light of a recent Twitter feud between comedian/pontificator Owen Benjamin and economist/Bitcoin maximalist Saifedean Ammous:

Bitcoin Isn’t Money (at Least Yet)

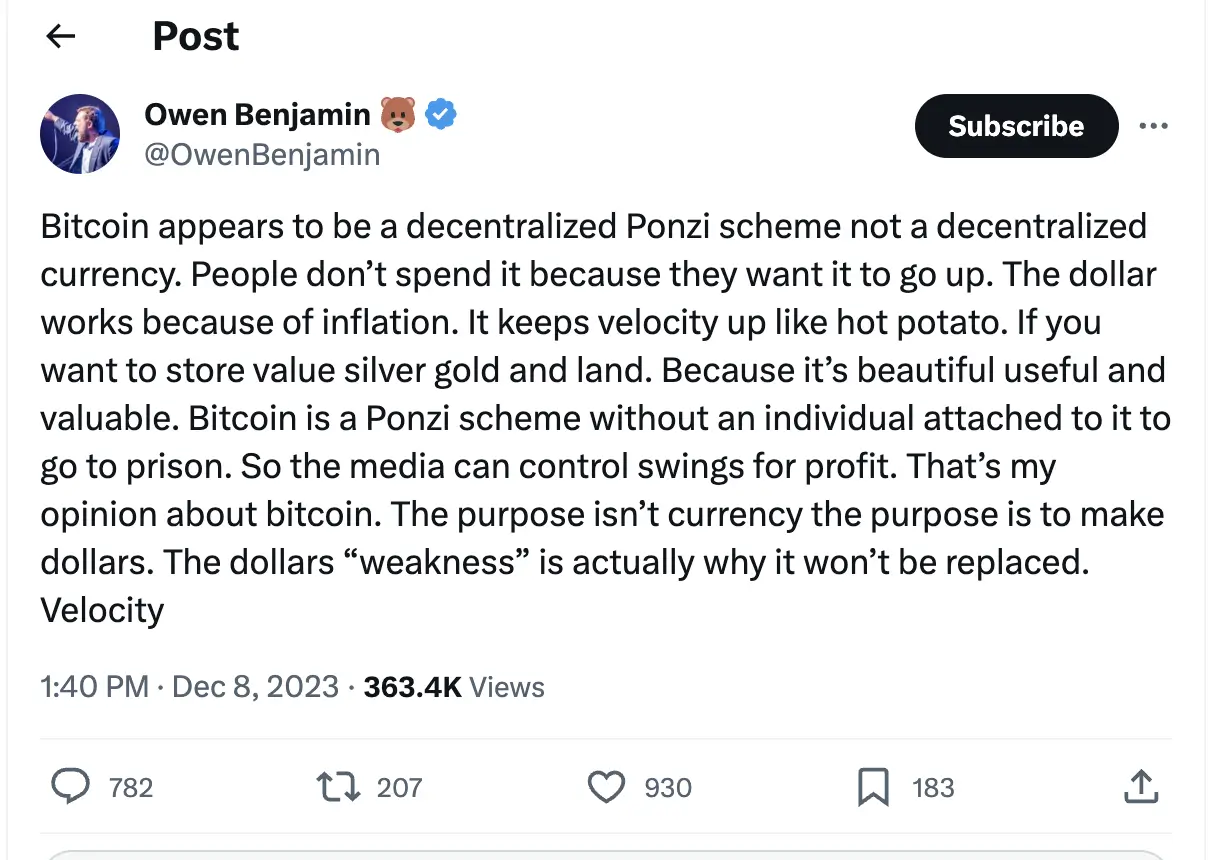

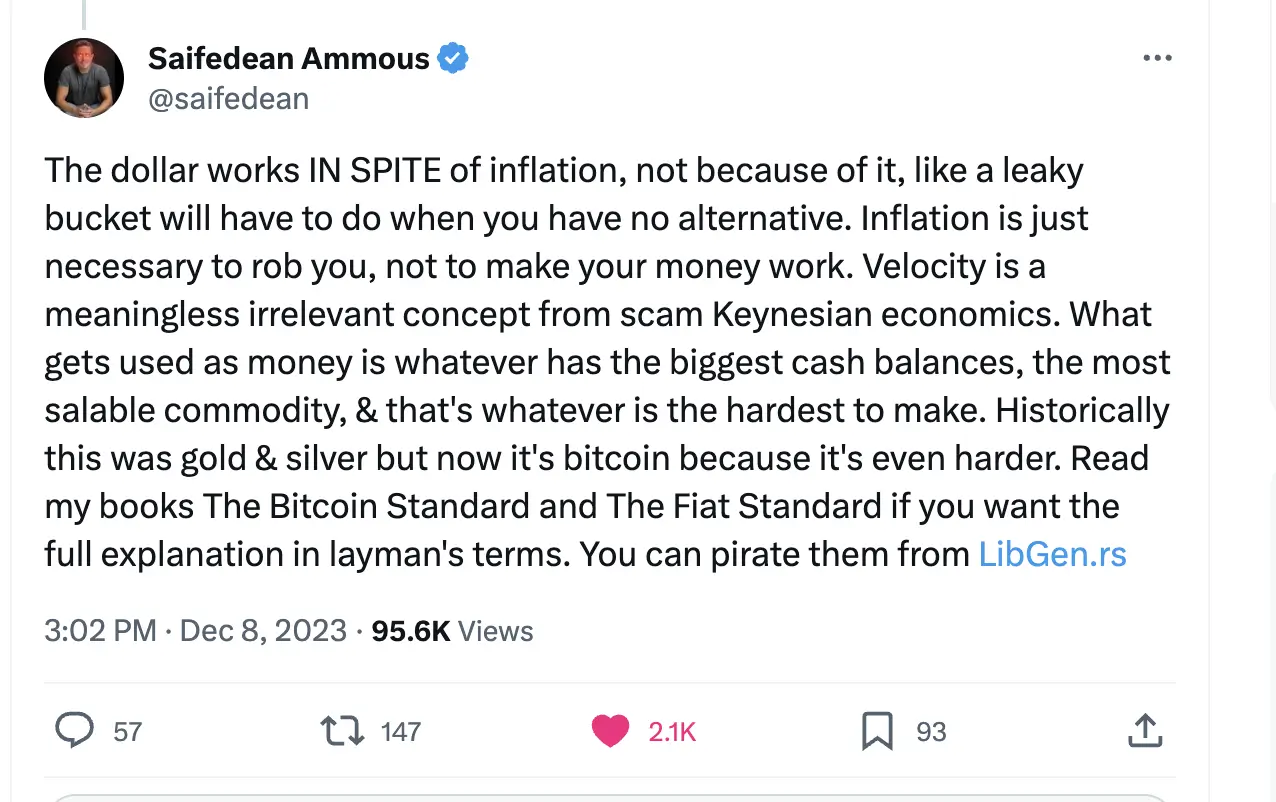

Like a good economist, I will give a two-handed reaction to the above exchange (which I have edited for space constraints, they each said more of course). On the one hand, I agree with Owen that right now Bitcoin is not money.

I use the standard definition of these terms as codified in the work of Ludwig von Mises, and as such, Bitcoin is clearly a medium of exchange, meaning that some people right now accept Bitcoin in trade not because they want to directly consume it, or even to use it to produce something else, but solely to hold it with the purpose of selling it in the future. But for a good to be classified as money, it must be a medium of exchange that is generally accepted in the community. On this criterion, I don’t think Bitcoin has yet passed the threshold, and as such I don’t think it yet qualifies as genuine money, though it might one day in the future.

A Good Money Maintains Its Purchasing Power

On the other hand, I agree with Saifedean that its inflationary aspect is a weakness of the US dollar. The reason the dollar became the global reserve currency is that it historically had been a relatively secure “store of value,” by which we simply mean that it maintains its purchasing power (or exchange rate vis-a-vis other goods and services) over time.

There is a long and nuanced history of the US dollar’s ties to gold and silver (which I briefly outline in a chapter in this online book). Suffice it to say, the dollar achieved its vaulted status not because it was always bleeding away its purchasing power, but rather because it was a relatively dependable currency that maintained its exchange value.

In the real world, when a country is wracked by hyperinflation, the citizens will abandon their domestic currency and either revert to barter, or they will conduct their transactions with a foreign currency. When making such a switch, they obviously don’t import a currency that has a 40% inflation rate; that’s the very type of disaster they’re trying to escape.

Unpacking Gresham’s Law

There’s a famous aphorism in economics called Gresham’s Law, which states that “bad money drives out good.” That seems to be what’s driving Owen’s comments quoted above.

However, this observation doesn’t mean that given a free choice, consumers will embrace bad money. That would be as nonsensical as claiming that “bad hamburgers drive out good” or “bad computers drive out good.” In every other area of commerce, we expect people to prefer good products over bad ones.

No, what Gresham’s Law referred to was a situation in which the government had enacted price controls and/or legal tender laws, which forced merchants to accept a certain money with a purchasing power that deviated from what the actual market equilibrium would have yielded. For example, during the early days of the US Republic, the official monetary policy was one of “bimetallism,” in which people could take raw gold or silver and have them stamped into official coins of particular denominations of US dollars. Because the very definition of “a US dollar” was stated in grains of gold or grains of silver, the government was effectively setting a price control, especially in conjunction with a legal system that would recognize certain items as being valid legal tender for the payment of debts.

In such an environment, when the actual market price of gold versus silver moved above or below the ratio that the US government policy had implicitly enshrined by law (with its two-fold definition of the dollar), it would give people an incentive to hoard one type of coin and spend the other. In other words, all of the merchants were charging in terms of dollars (and cents). So if the government then dictated how much gold or how much silver somebody had to come up with to qualify as dollars (or cents), people would naturally use the cheaper metal (in terms of the international market prices of them) when making their purchases.

For a modern analogy, consider: Suppose you want to buy something at the store that costs $1. You put your hand in your pocket and pull out five quarters. Four of the quarters were minted after the year 2000, but you look closely and realize that one of the quarters was minted in 1940, back when a quarter was 90% silver. Depending on the spot price of silver, that means a 1940 quarter is worth at least $5 and possibly much more, if it is in good condition and might appeal to collectors.

In this situation, you would be foolish to use your 1940 quarter in the transaction, where it will only be valued at the official “legal tender” price of 25 cents. So you would hoard that “good” quarter, and spend the four “bad” quarters, to buy the item marked at $1. Everybody else in the community is doing the same thing, and so people would conclude that Americans only use “bad quarters” as their money, which had driven out the “good quarters” from circulation.

So this is the pattern that Gresham’s Law is describing, but again, notice how particular this outcome is: It depends on the fact that we are all (in the United States) using US currency as defined by the authorities, and where someone can pay a debt denominated in dollars with quarters minted in the year 2000 even though they have no silver content.

Bitcoin Can Be a Good Money

As Saifedean stresses in his work, the fact that the total supply of bitcoins is ultimately capped at 21 million is a reason to favor it, in contrast to government-issued fiat currencies that can be doubled overnight by political whim.

We can imagine a scenario where everyone in society uses a money that is fixed in quantity, and therefore tends to gently appreciate year after year as the output of “real” goods and services continues to increase. In this framework, you would see the price of haircuts and hamburgers—quoted in satoshis—falling (say) 3 percent annually.

Contrary to Owen’s perspective, this pattern would NOT cripple the economy. Once people had adjusted to this pattern, interest rates and other prices would adjust. Right now, the price of buying 1MB of computer RAM drops even when measured in US dollars, but that doesn’t paralyze computer sales.

It’s true, if we’re starting off in a position when nobody wants to “spend” their bitcoins because they are holding them for speculative purposes, then it is not suitable as a generally accepted medium of exchange. But that is simply describing what happens in a transition period, as the purchasing power of Bitcoin rises to the level that its “fundamentals” (in terms of serving its role as a facilitator of trades) suggest. For those interested in more details on how this process of HODLing-leading-to-widespread-adoption-and-then-unloading could unfold, I refer you to this episode of my podcast.

Finally, I want to stress that I am not here predicting that Bitcoin, with or without augmentation from something like the lightning network, will one day become the money of planet Earth. Instead I am just trying to clarify the dispute that Owen and Saifedean had on Twitter, to give the economic framework in which to interpret their claims.

NOTE: This article was released 24 hours earlier on the IBC Infinite Banking Users Group on Facebook.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Twitter: @infineogroup, @BobMurphyEcon

Linkedin: infineo group, Robert Murphy

Youtube: infineo group

To learn more about infineo, please visit the infineo website